Emerging dynamics of Transaction Banking systems

Transaction banking is one of the fastest growing lines of business in corporate banking.

There is a wide variation in the capabilities of technology solution vendors, and so it is

imperative to have a well-designed approach to system selection and deployment

Transaction banking is one of the fastest growing segments in corporate banking, growing at CAGR of about 10% and is expected to account for 30-40% of corporate banking revenues by 2021. The key driver for this growth is the low cost of capital required for transaction banking, and the opportunity to enhance customer retention and cross-sell.

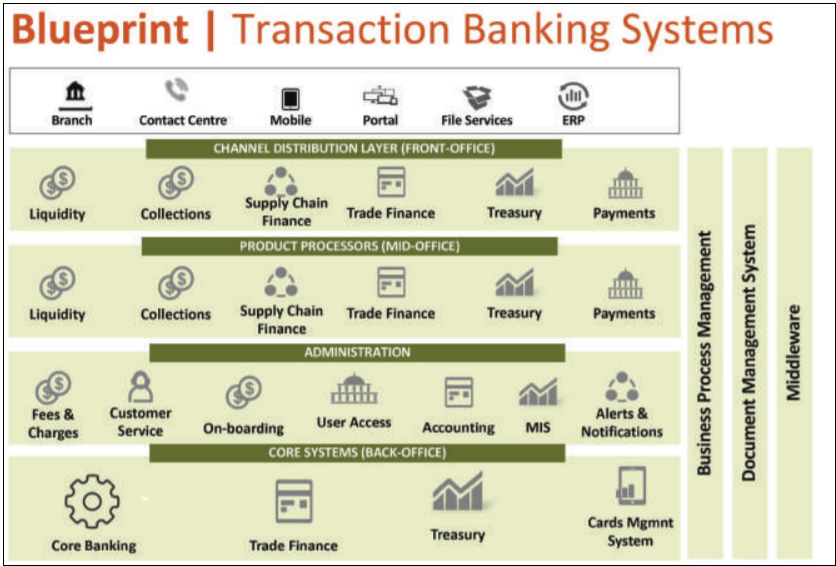

Transaction banking service portfolio

Essential services provided by leading transaction banking units are as follows:

• Liquidity management: Large corporate customers typically tend to have multiple banking relationships for convenience and diversification of exposure. However, this leads to fragmentation of their deposits, and unnecessary charges and fees. By offering liquidity management solutions such as sweeping, netting and pooling, banks can incentivise clients to consolidate their banking relationships with them. In the past, liquidity management services were constrained by the need for delivering liquidity management instructions to the bank in written form. But with the improvement of e-banking channel capabilities, it is possible for corporate clients to self-manage liquidity on their accounts and get a consolidated view of their financial position. Hence there has been a rapid growth in adoption of liquidity management solutions.

• Collections & receivables: For corporate customers who deal with a large volume of collections, it is inconvenient to track their status through in-house tools, since it leads to significant reconciliation effort. Some innovative solutions have emerged to address this issue. By offering cash collection, direct debit services and virtual accounts, banks can facilitate the tracking of collections and ensure that the proceeds of collections are retained with them. Advanced MIS capabilities, alerts and trackers make it very easy for customers to optimise their days of sales outstanding (DSO).

• Trade finance: Trade finance services have traditionally been a standard service with very few opportunities for differentiation. However, offering trade services to SME customers can often be unproductive. So banks are now offering trade finance portals to move at least part of the operations into a self-service model. Even though there is still a high dependence on physical documentation, new technologies such as blockchain will dramatically accelerate innovation in trade finance.

• Payments: Payments is easily the fastest evolving area of transaction banking. The two key primary drivers for innovation in the payments domain are the need for speed and the need for compliance to anti-money laundering (AML) and know-yourcustomer regulations. Large corporate customers expect banks to integrate with their ERP platforms to fully automate the payment process, and at the same time need support to ensure compliance with AML requirements. Some innovations such as B2B Platforms and payment hubs have been developed as a result.

• Supply chain finance: One of the fundamental purposes of banks is to facilitate trade and commerce for the growth of economies. Supply chain finance contributes to this by bringing together the buyers and sellers on a common platform. Banks have hitherto not been able to lend to small suppliers due to inability to verify their creditworthiness. Supply chain finance enables banks to lend to these suppliers on the strength of the buyer’s credentials. This a win-win for all stakeholders: banks can widen their credit footprint; suppliers can get better credit terms; and buyers can get better negotiating leverage with their suppliers. Governments also find this a potential tool to grow SMEs.

• Treasury services: Treasury services have been relatively slow in adopting new transaction banking technologies. The need for direct interaction between the customers and treasurers for advisory services dissuades customers for adopting self-service models. However, Transaction banking platforms can still be useful to give corporate treasurers valuable MIS and decision support.

Adopting Transaction banking capabilities

The commercial potential of Transaction banking has made it imperative for banks to adopt transaction banking systems and integrate them into their IT portfolio. In the last few years, liquidity management, payments and supply chain financing are experiencing rapid technology innovation. Unlike mainstream lending products, Transaction banking services are high-volume, so it is critical to leverage technology and automation to achieve efficiency of operations. Banks that have not yet invested in transaction banking platforms tend to experience the following challenges:

- Liquidity management: Lack of capabilities for netting, pooling and sweeping.

- Collections & receivables: Digital channel unavailable for managing receivables.

- Trade finance: No self-service capabilities for customers.

- Payments: Menu-based legacy interface for payments.

- Supply chain finance: No technology front-end and product predecessor platforms.

- Treasury services: Preference of phones and emails over online portals.

In the last few years, technology vendors have realised the potential for transaction banking and have developed innovative products targeted at this line of business. Supported by these platforms, transaction banking services are rapidly becoming automated and are witnessing the higher adoption of self-service models.

Developing transaction banking systems

Technology vendors offer distinct products for each component of the blueprint, which makes it convenient for banks to prioritise the roll-out of Transaction banking capabilities. However, wellestablished banks with legacy Core Banking platforms experience difficulties in implementing Transaction banking capabilities. Typically such banks already have legacy system capabilities addressing these requirements (such as liquidity management and payments), and hence their challenge is to implement the new platforms and weave them seamlessly into the legacy portfolio. The CIO of a bank typically has the following options for a transaction banking blueprint:

Option 1: Extend their current e-banking solution

Most banks already have robust e-banking capabilities for their retail business. They could extend the same capabilities to Transaction banking. This will ensure continuity of user experience and optimisation of investments for front-end channels. However, technology vendors who are good at e-banking solutions need not be good at offering the back-end capabilities required for supply chain, trade finance and payments. Hence the capabilities of the technology vendor for current e-banking will need to be carefully evaluated before deciding on this option.

Option 2: Extend the Core Banking platform

In order to have a good back-end platform, one of the available options is to adopt transaction banking modules from the current core banking technology vendor. However, not all core banking vendors provide transaction banking solutions. There may be a need to significantly customise the core banking platform to fill critical gaps. This approach is not advisable for a fast-evolving domain since it will result in significant overheads for managing the customisations and catching up with latest innovations.

Option 3: Implement a separate end-to-end transaction banking solution

Specialised transaction banking solutions are now available, though they may not have equally strong capabilities across the six domains of transaction banking. To select the right platform, banks will need to design a clear strategy for transaction banking and prioritise the modules that they would like to roll out in a phased approach. Also, banks will need to carefully evaluate their ability to integrate the transaction banking systems within their portfolio. An information management architecture will also need to be designed for sharing of customer master data between core systems and the Transaction banking platform.

In conclusion, deployment of transaction banking capabilities will need to be determined by a collaborative approach between business and technology teams of the bank. A good understanding of the vendor’s capabilities and their roadmap for transaction banking are essential for ensuring the successful roll-out of transaction banking systems.

For a further conversation on this subject of Cedar View or how we may be able to help please email V. Ramkumar, Senior Partner, Cedar at V.Ramkumar@cedar-consulting.com